-

-

Setting the right course

-

Do what you do best,

and leave pay-roll to us -

We will handle your accounting while you handle your business

-

over 200 specialists

BPG Polska- Your Partner in Business

We would like to present you the BPG Group and show the areas of possible cooperation in Poland and worldwide.

You are welcome to find out more about us and use services of BPG Group.

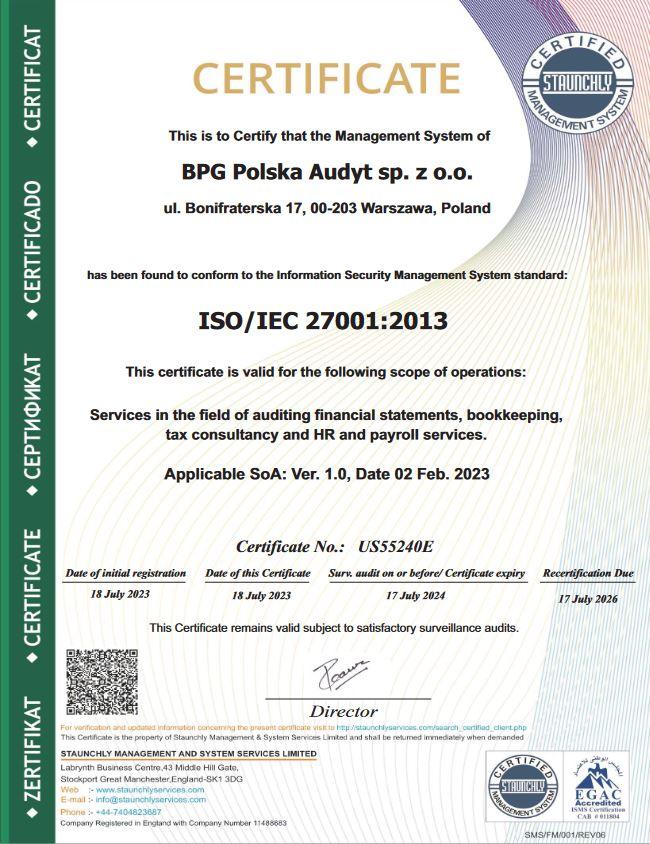

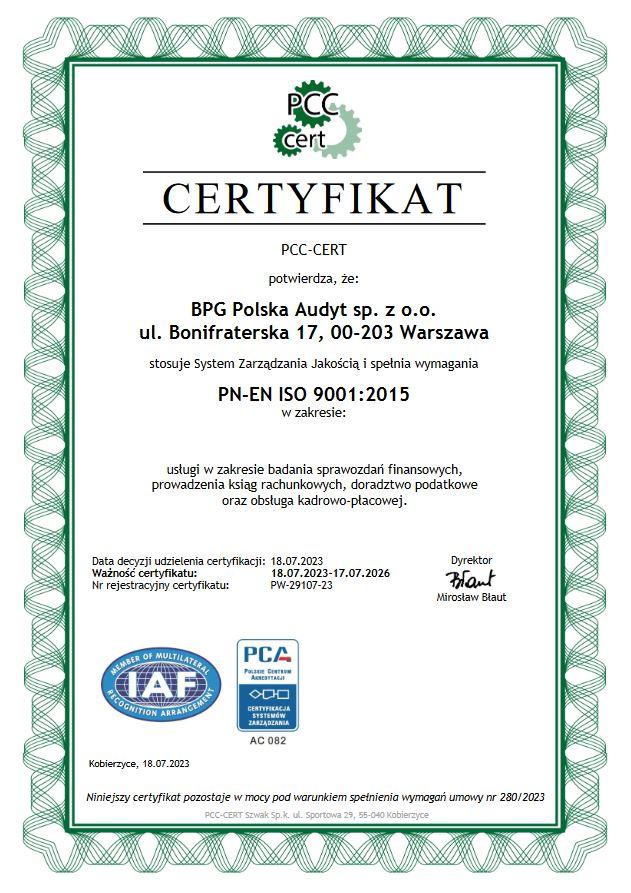

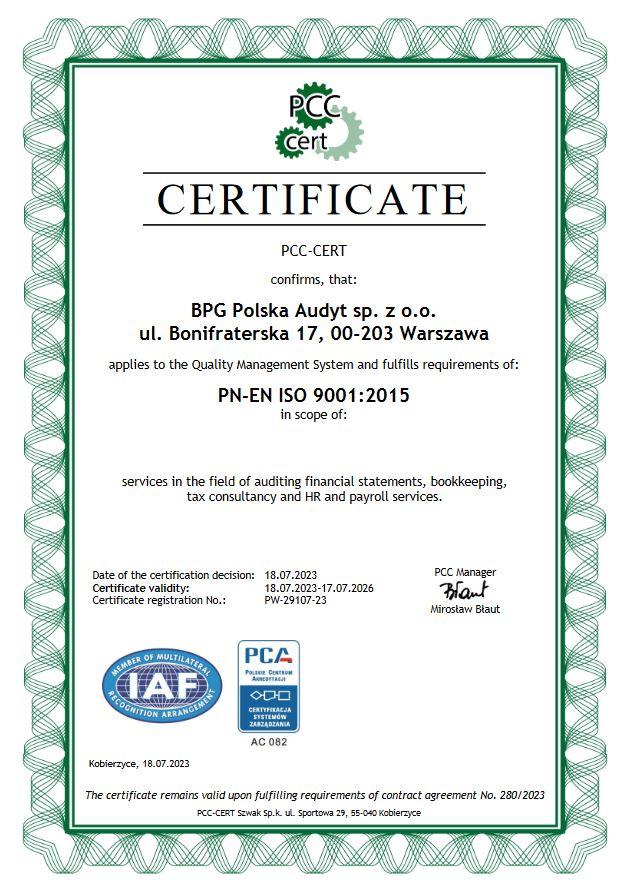

BPG Poland specializes in: audit of financial statements prepared in accordance with Polish law and IFRS, HGB, US GAAP, as well as other accounting standards, tax advisory, ledger keeping, payroll and personnel, as well as related services for companies and enterprises with various status of business, as well as for natural persons.

We are members of Kreston International